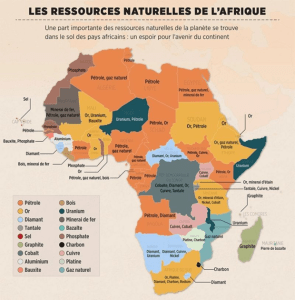

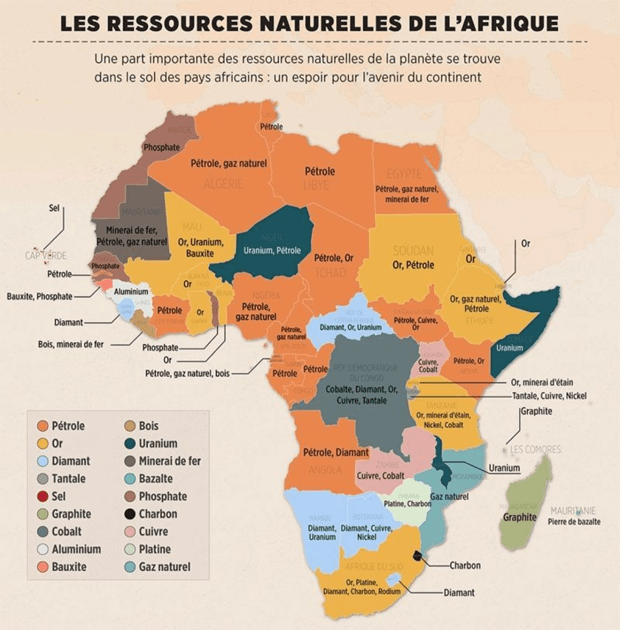

In the context of increasing global competition for energy and critical metals, Africa is gradually establishing itself as a central geoeconomic player. Long perceived as a mere extractive periphery, the continent now occupies a strategic position in global energy and industrial security.

In the north of the continent, Algeria, Libya, and Egypt constitute a major energy hub. Their hydrocarbon resources contribute significantly to the energy supply of Europe and, to a lesser extent, some Asian economies. Further south, the Gulf of Guinea, dominated by Nigeria and Angola, remains one of the main oil-producing regions in Africa. However, these areas remain vulnerable to maritime shocks and fluctuations in international prices.

To the east and center, another strategic area is emerging: the Democratic Republic of Congo – Zambia – Tanzania axis. This region contains significant reserves of cobalt, copper, and tantalum, minerals essential for manufacturing batteries, digital technologies, and the infrastructure of the global energy transition.

In the south, South Africa and Namibia, alongside Niger, are participating in the integration of the continent into strategic nuclear and metallurgical supply chains thanks to their uranium and industrial mineral resources.

However, a structural weakness persists: the low value capture associated with the raw export of resources. The major challenge for Africa no longer lies solely in the possession of deposits, but in the capacity to develop local processing chains, efficient logistics corridors, and genuine regional technological sovereignty.