One of the most common mistakes investors and entrepreneurs make is viewing Africa as a single market. This simplification, while tempting, can be costly. The African continent comprises 54 countries, each with its own unique economic, regulatory, and technological realities. Ignoring this diversity means underestimating the complexity of the opportunities—and the risks.

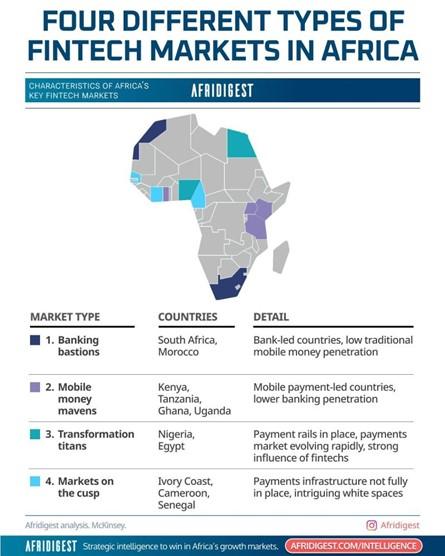

In the fintech sector, this reality is particularly evident. Africa is not developing according to a uniform model, but rather through several types of markets, each structured by its level of financial infrastructure. At least four major archetypes can thus be identified, which directly influence the strategies to be adopted.

In countries like South Africa and Morocco, often referred to as “banking strongholds,” financial systems are already well-established. Traditional banks largely dominate, and any innovation must fit within this structured environment. Fintech products must, above all, inspire trust and offer real added value to compete with established institutions.

Conversely, countries like Kenya and Ghana embody the model of “mobile money pioneers.” Here, telecom operators play a central role in financial services. Mobile payment solutions are deeply ingrained in consumer habits. In these markets, a company that fails to integrate with existing mobile money systems risks simply remaining invisible.

Other economies, such as Nigeria and Egypt, represent “rapidly transforming markets.” These environments are characterized by strong entrepreneurial dynamism, where fintech startups actively participate in shaping the economy. Innovation is rapid, competition intense, and opportunities abound for players capable of adapting.

Given this diversity, it is clear that no one-size-fits-all strategy can work. An approach that is effective in Lagos will not necessarily be relevant in Nairobi. Success depends on a thorough understanding of local infrastructure, user behavior, and regulatory frameworks.

This does not mean, however, that the continent’s integration should be ignored. On the contrary, initiatives like the African Continental Free Trade Area (AfCFTA) are paving the way for the gradual harmonization of markets. The development of the Digital Trade Protocol and the Pan-African Payment and Settlement System (PAPSS) represents a major step towards interconnecting African economies.

However, this integration remains a long-term objective. The current reality is that of a fragmented continent, where each market must be approached individually. To succeed in 2026, companies must adopt a so-called “dual-track” strategy.

On the one hand, it is essential to respect the specific characteristics of each market by adapting products and business models to local infrastructures. On the other hand, it is equally important to prepare for the future by developing technological solutions capable of operating on a regional scale, in anticipation of increased integration.

Ultimately, capital alone is not enough to succeed in Africa. Understanding the context is crucial. Companies that can navigate between local adaptation and a continental vision will be best positioned to capitalize on Africa’s potential. Africa is not yet a unified market, but it is gradually moving in that direction—and it is precisely in this transition that the greatest opportunities lie.